New data reveals students in the U.S. lack financial savvy; higher ed, economy should worry

Editor’s note: This story has been updated to reflect changes in data.

Editor’s note: This story has been updated to reflect changes in data.

According to an upcoming report from Junior Achievement and PwC, nearly a quarter of today’s students believe that after they complete college their student loan debt will be forgiven. Yet, 41 percent default on their loans. There’s a financial literacy disconnect going on between reality and today’s students, but it’s not just worrisome for bank accounts—it’s affecting colleges, business and the global economy.

In the Organization for Economic Co-operation and Development’s (OECD) latest global assessment, more than 1 in 6 U.S. teens are unable to make even simple decisions about everyday spending, and only 1 in 10 can solve complex financial tasks.

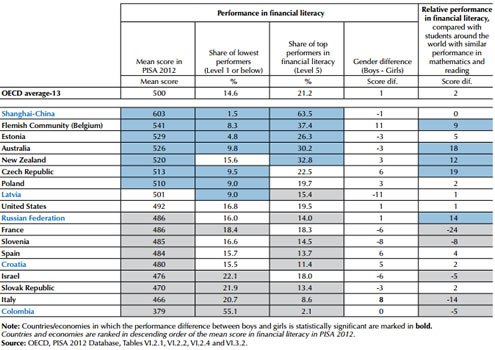

The OECD’s PISA Financial Literacy assessment, which tested the knowledge and skills of teenagers in dealing with financial issues, such as understanding a bank statement, reveals that U.S. students perform around the average of the countries and economies that participated, ranking somewhere between 8 and 12.

Shanghai-China had the highest average score in financial literacy, followed by the Flemish Community of Belgium, Estonia, Australia, New Zealand, the Czech Republic and Poland (larger view available in the report):

29,000 15 year-old students in 18 countries and economies were tested with the assessment through a 60 minute paper-based test. Students were also asked to participate in a math and reading assessment, and to provide information on their backgrounds, attitudes towards learning, and experience with money and financial products. In the U.S., 1,133 students in 158 schools completed the assessment.

But what’s most interesting about the data is the extreme correlation that happens between other skills for students in the U.S.

Data revealed that skills in mathematics and reading are very closely related to financial literacy, more so in the U.S. than in other countries: Around 80 percent of the financial literacy score reflects skills that can be measured in math and/or reading assessments (compared with the OECD average of 75%), while 20% of the score reflects factors that are uniquely captured by the financial literacy assessment (compared with the OECD average of 25%).

(Next page: What this means for colleges and business)

Only 9.4 percent of U.S. students performed at the “highest level,” which is similar to the average of 9.7 percent across OECD countries. “These top performers can look ahead to solve financial problems or make the kinds of financial decisions that will be only relevant to them in the future,” explained the OECD. “They can take into account features of financial documents that are significant but unstated or not immediately evident, such as transaction costs, and can describe the potential outcomes of financial decisions.”

But why is nine percent financial literacy troubling? Shannon Schuyler, Partner and U.S. Leader for Corporate Responsibility, PwC, has some thoughts.

Schuyler, who led PwC’s launch of Earn Your Future (EYF) in 2012, a commitment to invest $160 million in cash donations and volunteer hours to youth education through 2.5 million students and educators over five years, says the worry starts with the aging population.

“It’s interesting to see, in these megatrends, what demographics are showing us: By 2050….22% of the world’s population will be age 60 or older. (Source: UN Department of Economic and Social Affairs, Population Division, Population Ageing and Development 2012, 2012), leaving a large gap in skilled jobs—a gap that many companies are nervous about filling due to concerns about student skills,” she explained.

Schuyler noted that knowing financial skills isn’t just about balancing a checkbook, it’s about using critical thinking skills to analyze and solve a problem.

“What the lack of financial literacy shows us is that students don’t just lack personal finance skills, it’s also lack of mathematics, critical thinking and reading comprehension,” she emphasized. “There’s a large correlation to math and reading in the U.S., more so than in other countries, which means that not only should students have better math and reading skills, financial literacy can be a major way to teach those math and reading comprehension skills.”

Outside of business concerns and the lack of skilled workers, another major concern is that financial literacy isn’t required in schools and colleges as part of the curriculum, which, explained Schuyler, is due in part because no one talks about personal finances.

“While the vision is to have a great curriculum that can be taught and assessed in schools, a general curriculum has yet to be designed, and most teachers don’t have the skills necessary to teach financial literacy,” she said. “This is partly because it’s considered taboo in our society to talk about personal finances, so kids aren’t talking about it with their parents, and teachers aren’t talking about it in their training. Businesses and teacher colleges can step up to help educate teachers.”

(Next page: Why this affects higher ed)

Also troubling is the affect the lack of financial literacy skills has on the current national student loan debt crisis, which not only affects the legitimacy of degrees and institutions, but the stability of the economy as well.

“Part of being financially literate is also understanding how student loans work: According to data, nearly a quarter of students surveyed believe that their student loan debt will be forgiven after they graduate; yet, 41 percent of all students default on their loans,” noted Schuyler. “There needs to be a triangulation between career choice, college choice and degree choice that doesn’t exist for students today. Financial literacy will help with these decisions.”

Indeed, knowing how to apply math and critical thinking skills to a college decision is critical for today’s students, including understanding how tuition directly correlates to student loan interest and base salaries in careers.

Not only could this help students from defaulting on their loans, but higher education (currently under intense public scrutiny), may better understand how to serve students and help provide pipelines to critical jobs in the business industry.

- 25 education trends for 2018 - January 1, 2018

- IT #1: 6 essential technologies on the higher ed horizon - December 27, 2017

- #3: 3 big ways today’s college students are different from just a decade ago - December 27, 2017

Comments are closed.